Dubai Property Replacement Cost 2026: Why Today's Prices Are Tomorrow's Floor

Discover why Dubai property prices in 2026 are structurally supported by rising replacement costs. Expert analysis on prime real estate floors. Read now.

Dubai is the global capital of branded residences by pipeline volume per Knight Frank's Global Branded Residences Report, with the segment growing faster than any other Dubai luxury category over the last decade.

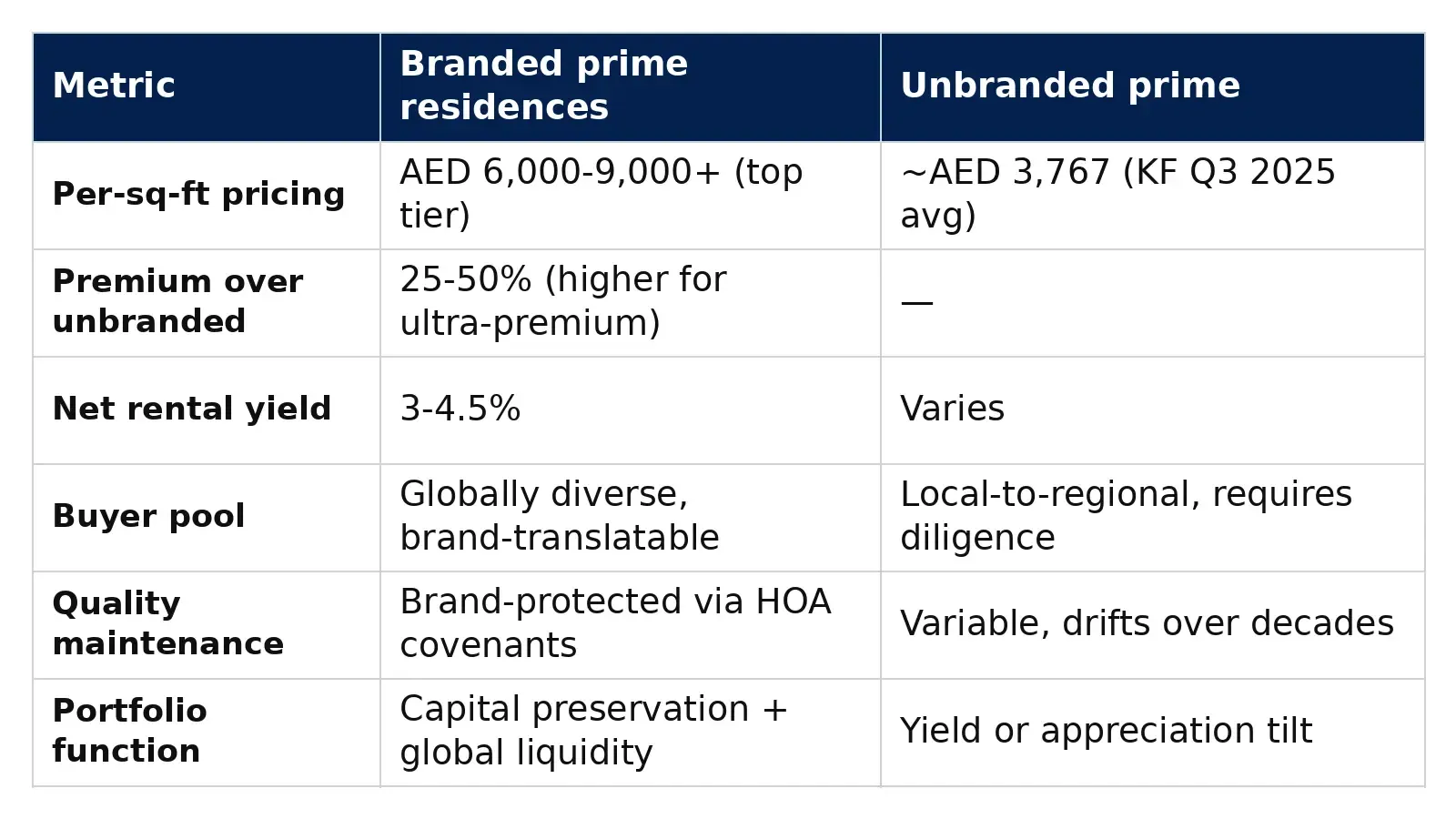

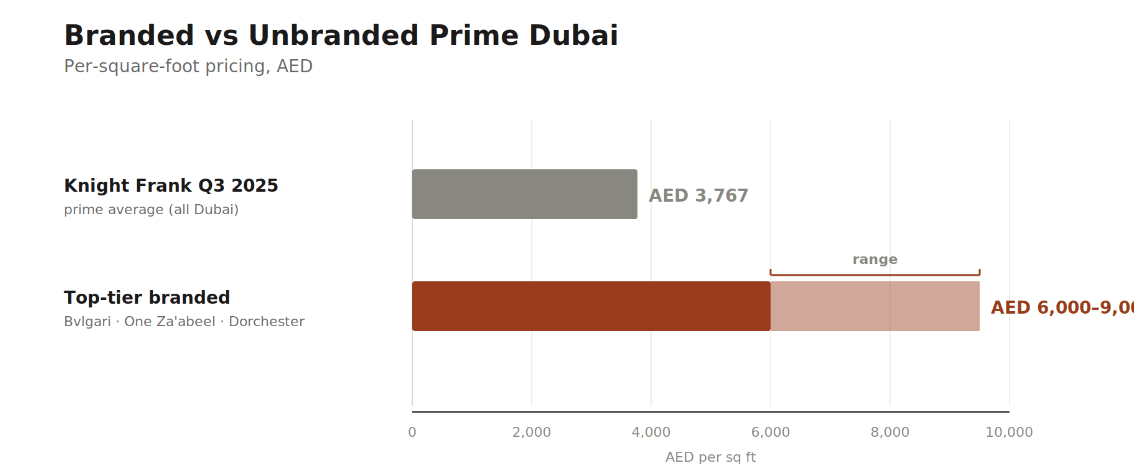

Branded residences typically transact at 25 to 50 percent premiums versus comparable unbranded prime product, with ultra-premium brands like Bvlgari and One Za'abeel commanding higher premiums.

The premium pays for four economic features that compound over a long hold: brand grade construction specification, hospitality grade service standard, globally diverse buyer pool, and continuing brand reputational stake in maintaining standards.

Bvlgari Residences on Jumeirah Bay Island, One Za'abeel, and the Dorchester Collection at Downtown have transacted at AED 6,000 to 9,000 plus per sq ft, against Knight Frank's Q3 2025 prime average of AED 3,767 per sq ft.

Branded residences function as preservation and optionality assets first, with net yields of 3 to 4.5 percent and the most stable risk adjusted return profile across cycles.

Branded residences are the fastest-growing segment of Dubai luxury real estate, and the only segment where the city has moved from regional player to global leader inside a single decade. Knight Frank's global tracking has consistently put Dubai at or near the top of the worldwide league table for branded residence pipeline, and the city accounts for a meaningfully larger share of global branded residence supply than its size would suggest in any other real estate category. As a property segment, this barely existed in Dubai in 2015. By 2026, it is one of the most active corners of the prime market.

My KHDA Luxury Brand Manager training, alongside time spent with Unilever earlier in my career working through the mechanics of how brand equity converts into pricing power, makes this segment particularly interesting to me. Branded residences are a specific kind of property structure where the analytical framework from luxury brand economics applies more directly than in any other real estate category. Most retail commentary on Dubai branded residences frames them as luxury apartments with a designer name attached. That framing misses what is actually being purchased, why the segment is growing the way it is, and why the institutional version of the analysis produces a meaningfully different conclusion from the retail version.

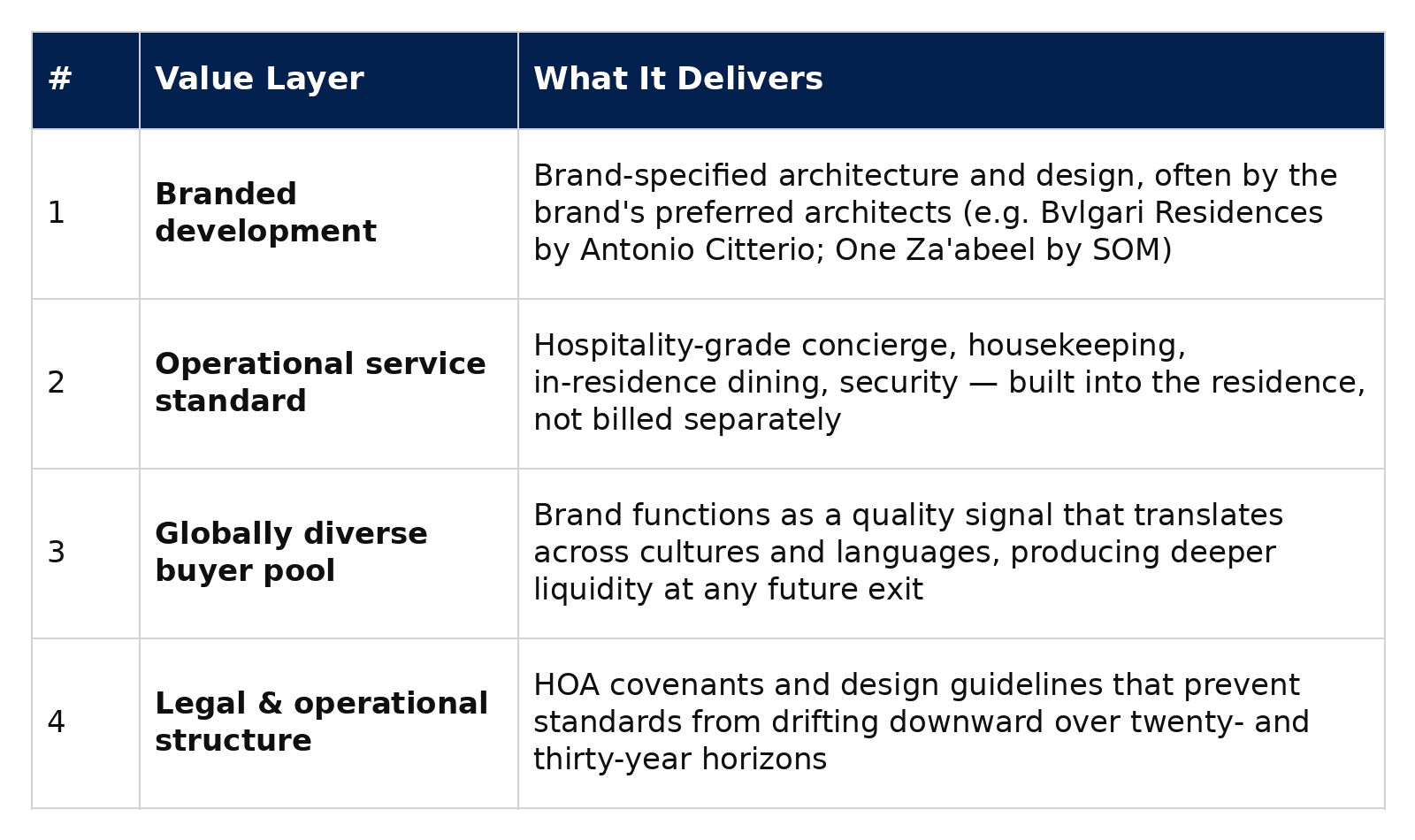

A branded residence is not just an apartment with a logo. It is a property structured around four distinct value layers that operate together.

The first layer is the branded development itself, designed and specified to the brand's standards, often by the brand's preferred architects and interior designers. Bvlgari Residences in Jumeirah Bay, designed by Antonio Citterio. One Za'abeel by SOM. The Dorchester Collection at Dorchester Residences. Each carries specifications, finishes, and design vocabulary that are not interchangeable with non-branded equivalents.

The second layer is the operational service standard. Most branded residences operate hospitality-grade service, often run by the brand's hotel operations team or a closely affiliated operator. Concierge, housekeeping, in-residence dining, security, and the broader hospitality stack are delivered to standards that ready-market apartments cannot easily replicate. The service is not a separate fee structure; it is built into the residence itself.

The third layer is the buyer pool. Branded residences attract a globally diverse buyer pool from dozens of jurisdictions because the brand functions as a quality signal that translates across cultures and languages. A buyer in Lagos evaluating Dubai property has no efficient way to assess the difference between two unbranded developments at similar price points. The same buyer evaluating Bvlgari Residences understands what they are buying because the brand transmits the standard. This diversity is itself a financial asset, the buyer pool depth at any future exit is meaningfully greater than for unbranded equivalents.

The fourth layer is the legal and operational structure that maintains the brand standard over time. Branded residences typically have HOA structures, design guidelines, and operational covenants that prevent the standard from drifting downward across decades. This is more important than retail commentary recognises, because it is the mechanism through which branded residences hold their relative pricing premium against the broader market over twenty- and thirty-year horizons. An unbranded development can drift in finish quality, common area maintenance, and tenant mix in ways that compress its premium. A branded residence is structurally protected against that drift by the brand's reputational stake.

Branded residences in Dubai typically transact at 25-50% premiums versus comparable unbranded prime product in the same submarket, with some ultra-premium brands commanding higher premiums.

Branded vs Unbranded Prime Dubai pricing chart

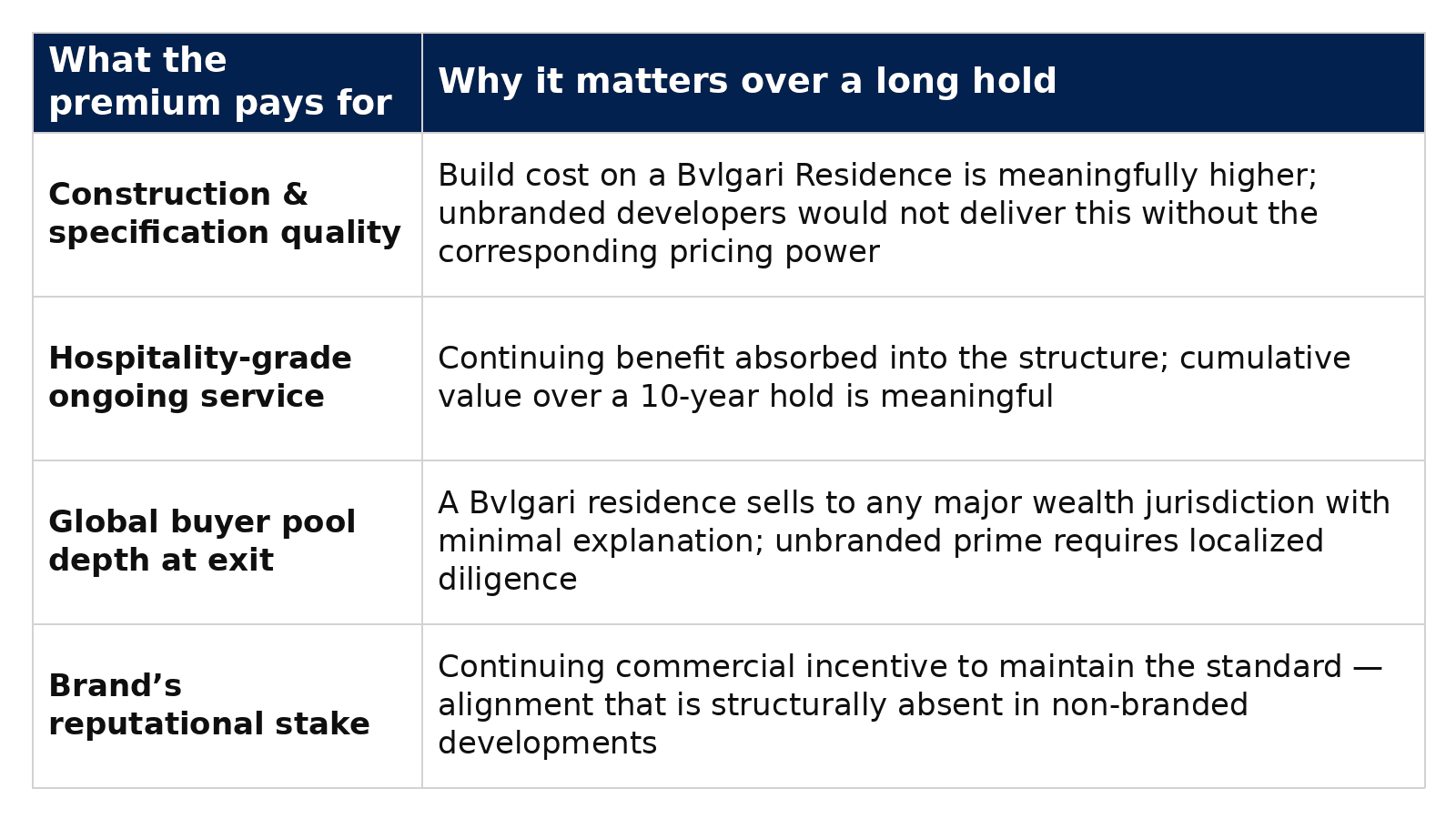

The retail framing is that the premium is paying for the brand label. The institutional framing is that the premium is paying for four specific economic features that compound over a long hold.

The premium pays for the construction-and-specification quality that an unbranded developer would not deliver at the same price point because they would not capture the corresponding pricing power. Build cost on a Bvlgari Residence is meaningfully higher than on a comparable unbranded prime apartment because the brand requires it.

The premium pays for the operational service standard, which is a continuing benefit rather than a one time amenity. Hospitality grade service costs are real and ongoing, and they are absorbed into the structure rather than billed separately. Over a 10 year hold, the cumulative service value is meaningful.

The premium pays for the global buyer pool depth at exit. A Bvlgari residence can be sold to a buyer in any major wealth jurisdiction with minimal explanation. An unbranded prime apartment requires the buyer to evaluate the specific developer, building, and finish standard, which compresses the buyer pool and produces wider bid-ask spreads at exit. The premium pays for the brand's continuing reputational stake in the development. The brand has a commercial incentive to maintain the standard because their global brand equity is on the line. This produces an alignment between the property owner and the brand operator that is structurally absent in non branded developments.

Branded residences serve specific portfolio functions, and the framework for thinking about them is different from yield-tilted or pure-appreciation positions. They are capital preservation assets first. The premium pricing, brand-protected quality maintenance, and globally diverse buyer pool produce structural support for the asset's value across cycles. They are not the highest-yield positions in a Dubai portfolio. Net yields typically run 3-4.5%, lower than mid-market apartments and modestly below typical prime villa stock. They are not the highest-appreciation positions either; the headline appreciation curves can underperform infrastructure-led growth corridors over specific windows.

What they are is the segment with the most stable risk-adjusted return profile across cycles. They hold through volatility, recover quickly, attract a deep buyer pool at exit, and provide a degree of capital preservation that other Dubai segments cannot match. For HNW capital where preservation and optionality matter as much as appreciation, the branded residence segment is structurally well-suited.

They also serve a specific lifestyle function for many HNW buyers. The hospitality-grade service makes the asset usable as a part-time residence without operational management overhead, which is particularly relevant for internationally mobile capital that wants Dubai exposure without full-time presence. The asset works as a primary residence, a winter base, an occasional family retreat, or a guest apartment, with the operational layer absorbing the management burden in each case.

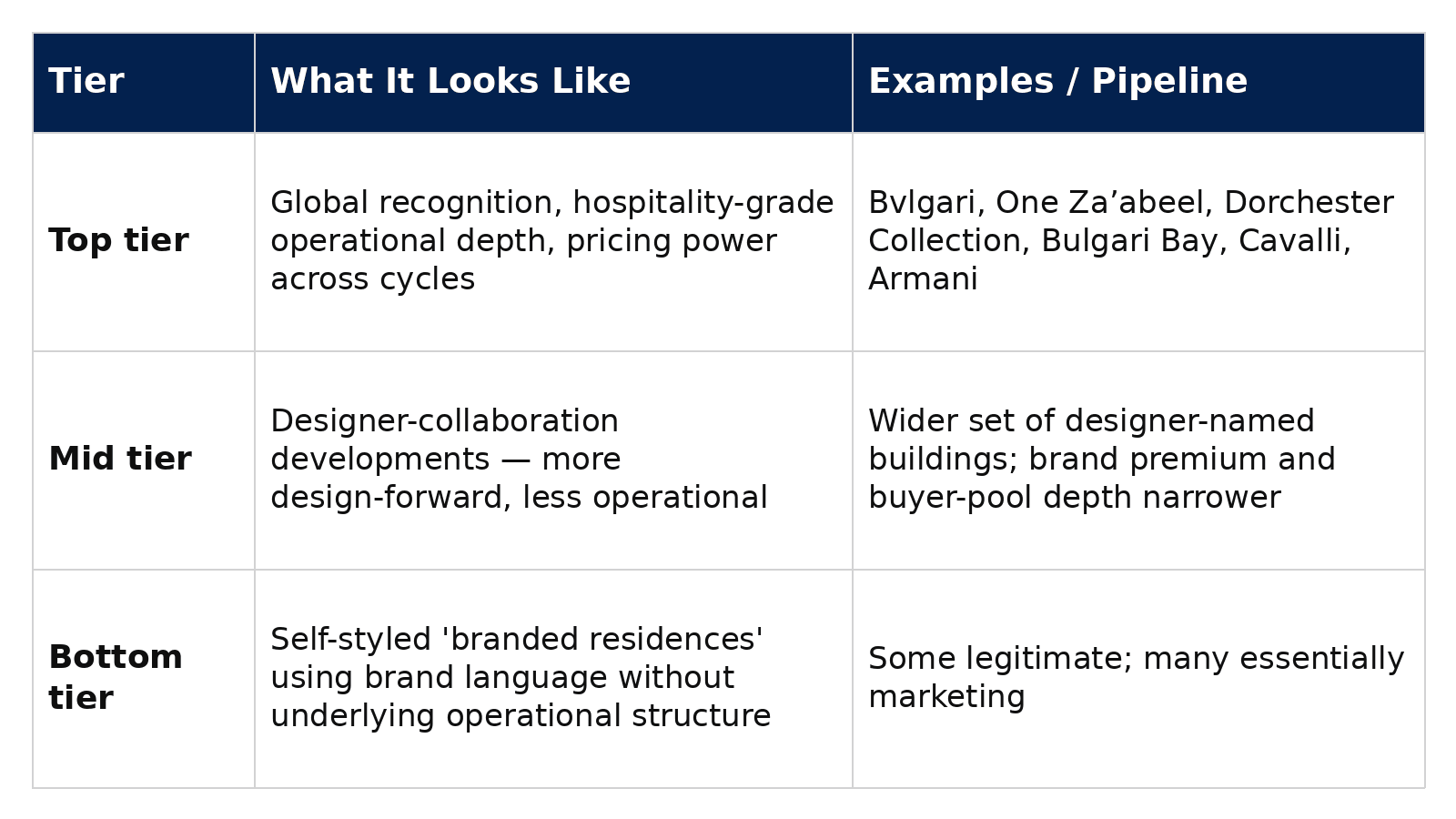

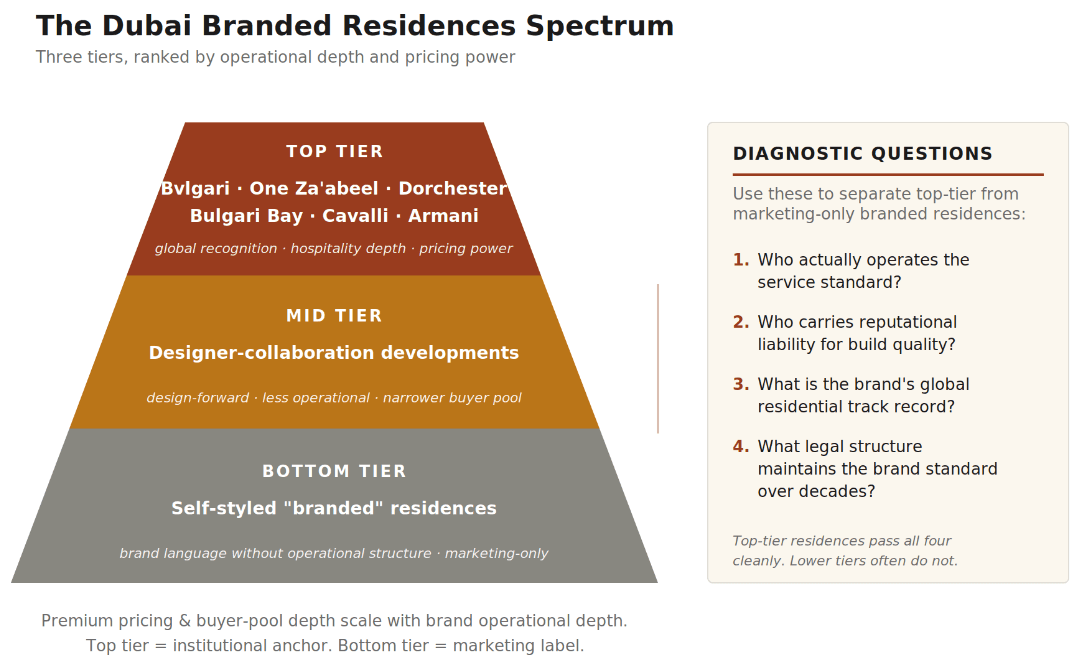

Not all branded residences are positioned equally, and the framework for evaluating them treats brand strength as a primary variable.

Dubai branded residences three-tier brand quality spectrum The segment is also accumulating new entrants quickly. Knight Frank tracks a meaningful pipeline of new branded residence launches in Dubai through 2026-2028, with luxury hospitality groups (Mandarin Oriental, Six Senses, Aman, Rosewood, Four Seasons) and luxury fashion houses (additional Bvlgari, Cavalli, Versace product) all expanding their Dubai residential footprint. The supply expansion is meaningful, but the demand pool is global and growing, and the supply concentration in genuinely top-tier brand-and-location combinations remains tight.

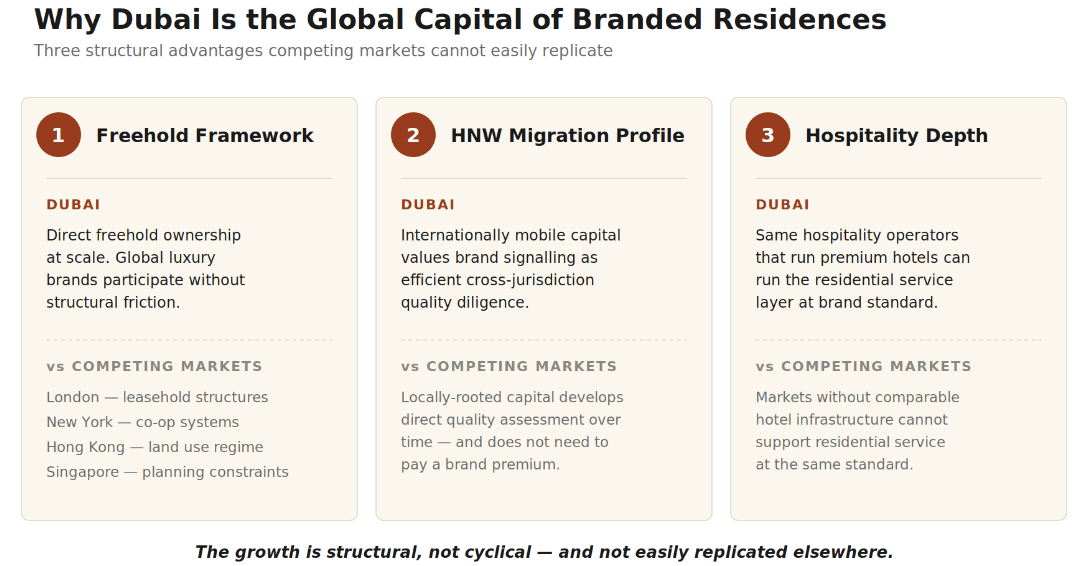

The reason Dubai has become the global capital of branded residences is structural rather than promotional, and understanding the structural reasons is part of the framework for evaluating the segment's durability.

• Freehold framework removes friction. Dubai’s freehold structure allows global brands to participate in residential development at scale without the complications London’s leasehold structures, New York’s co-op systems, Hong Kong’s land use regime, or Singapore’s planning constraints impose. • HNW migration profile maps to demand. Internationally mobile capital relocating from multiple jurisdictions places higher value on brand signalling than locally-rooted capital does. In Dubai, the brand premium is the efficient mechanism for translating global wealth into local property. • Hospitality infrastructure depth. The same hospitality operators that run the city’s premium hotels can run the residential service layer — operational depth that markets without comparable hotel infrastructure cannot match.

Three structural advantages making Dubai the global capital of branded residences. The combination of freehold framework, buyer pool match, and hospitality operational depth makes Dubai structurally well-suited to be the global capital of branded living. The growth is unlikely to be cyclical in the way most retail commentary frames it.

Within the branded residence segment, the entry framework is somewhat different from the broader Dubai market. The launch pricing on a top tier branded residence is typically the most efficient entry point relative to long term value, because the brand has incentives to set launch pricing at levels that produce strong absorption velocity to validate the development's positioning. Subsequent secondary market pricing typically rises into and through stabilisation, with the gap between launch pricing and ten year secondary pricing often substantial.

The window for accessing top-tier branded residence inventory at launch is narrow. These developments typically sell through allocations to known buyers, family office networks, and broker-curated pools rather than open public release. Capital that wants to deploy into the launch pricing tier needs to be in those networks before the development opens. By the time the development is publicly marketed, the entry tier allocation is usually closed. This is one reason serious Dubai-focused capital maintains active relationships with brokers who handle branded residence flow, even when not actively transacting. The information flow on upcoming launches is the variable that determines whether the capital can access the segment at the most efficient entry point.

Secondary market pricing in established branded residences (Bvlgari Jumeirah Bay, Armani Residences, the original Cavalli product) has firmed meaningfully through 2024-2026, with limited inventory typically transacting at premium to launch. The inventory that does come to secondary market is often estate-driven, divorce-driven, or relocation-driven rather than profit-taking, which means the deal flow is sporadic and requires patient deployment.

Branded residences are not an interesting niche in Dubai luxury real estate. They are the segment that will define the next decade of how prime Dubai property is structured, owned, and transacted.

The demand drivers (global wealth migration, brand translatable signalling, hospitality-integrated lifestyle) are structural rather than cyclical. The supply drivers (Dubai's structural advantages over competing prime markets) are not easily replicated. The buyer pool depth is global and growing.

For capital that is approaching Dubai as a long-horizon allocation rather than a short-term trade, the branded residence segment deserves more weight in portfolio construction than typical retail allocations give it. It is the segment that most cleanly fits the institutional brief of preservation plus optionality plus global liquidity. It is also the segment most insulated from the specific dispersion pressures that will affect mid-market product through 2026-2027.

Most Dubai investors will continue to read branded residences as a luxury accessory to their portfolio. The framework that drives sophisticated capital reads them as the structural anchor of a serious Dubai allocation, with the rest of the portfolio constructed around them.

The premium pricing is real. So is what it is buying. Over a decade, the segment is likely to compound at rates that retail commentary has not fully internalised, and the gap between the institutional and retail readings of it will continue to widen.

The Dubai Allocation is a 20-part research release published by Xperience Realty in May 2026, treating Dubai real estate as a capital allocation decision rather than a transactional one. The release functions as a 2026 mid-year house view, written for principals, family offices, and internationally mobile capital evaluating Dubai through the rest of 2026 and beyond. The full research package is available at xrealty.ae.

The Dubai Allocation is a 20 part research release published by Xperience Realty in May 2026, treating Dubai real estate as a capital allocation decision rather than a transactional one. The release functions as a 2026 mid year house view, written for principals, family offices, and internationally mobile capital evaluating Dubai through the rest of 2026 and beyond. The full research package is available at xrealty.ae.

Branded residences are luxury properties developed and operated under a luxury brand's name and standards. Dubai examples include Bvlgari Residences, One Za'abeel, Dorchester Collection, Bulgari Bay, Cavalli, and Armani Residences. They combine branded design and finish standards with hospitality-grade operational service.

Branded residences carry 25 to 50 percent premiums over comparable unbranded prime product because the premium pays for higher construction specification, hospitality-grade ongoing service, deeper global buyer pool depth at exit, and the brand's continuing reputational stake in maintaining the development's standard over decades.

Bvlgari Residences on Jumeirah Bay Island has transacted at AED 6,000 to 9,000 plus per sq ft, with strong secondary market firmness through 2024-2026. Limited inventory typically transacts at premium to launch pricing. The asset class is positioned for capital preservation and global liquidity rather than maximum yield.

Active in Dubai: Bvlgari (Jumeirah Bay Island), Dorchester Collection (Downtown), Cavalli, Armani (Burj Khalifa Residences), One Za'abeel, Bulgari Bay, with growing pipelines from Mandarin Oriental, Six Senses, Aman, Rosewood, Four Seasons, Versace, and additional Bvlgari product through 2026-2028.

Branded residences typically deliver 3 to 4.5 percent net rental yields, lower than mid market apartments and modestly below typical prime villa stock. Their portfolio function is capital preservation and global liquidity rather than current income, with the brand and service quality producing stable risk-adjusted returns across cycles.

Discover why Dubai property prices in 2026 are structurally supported by rising replacement costs. Expert analysis on prime real estate floors. Read now.

JP Morgan poured $20B into the Gulf with hundreds of billions more to come. See what it means for Dubai property investors. Read the full analysis.

Compare Dubai rental yields and capital appreciation in 2026. Learn how yield, growth and liquidity shape total returns across communities.