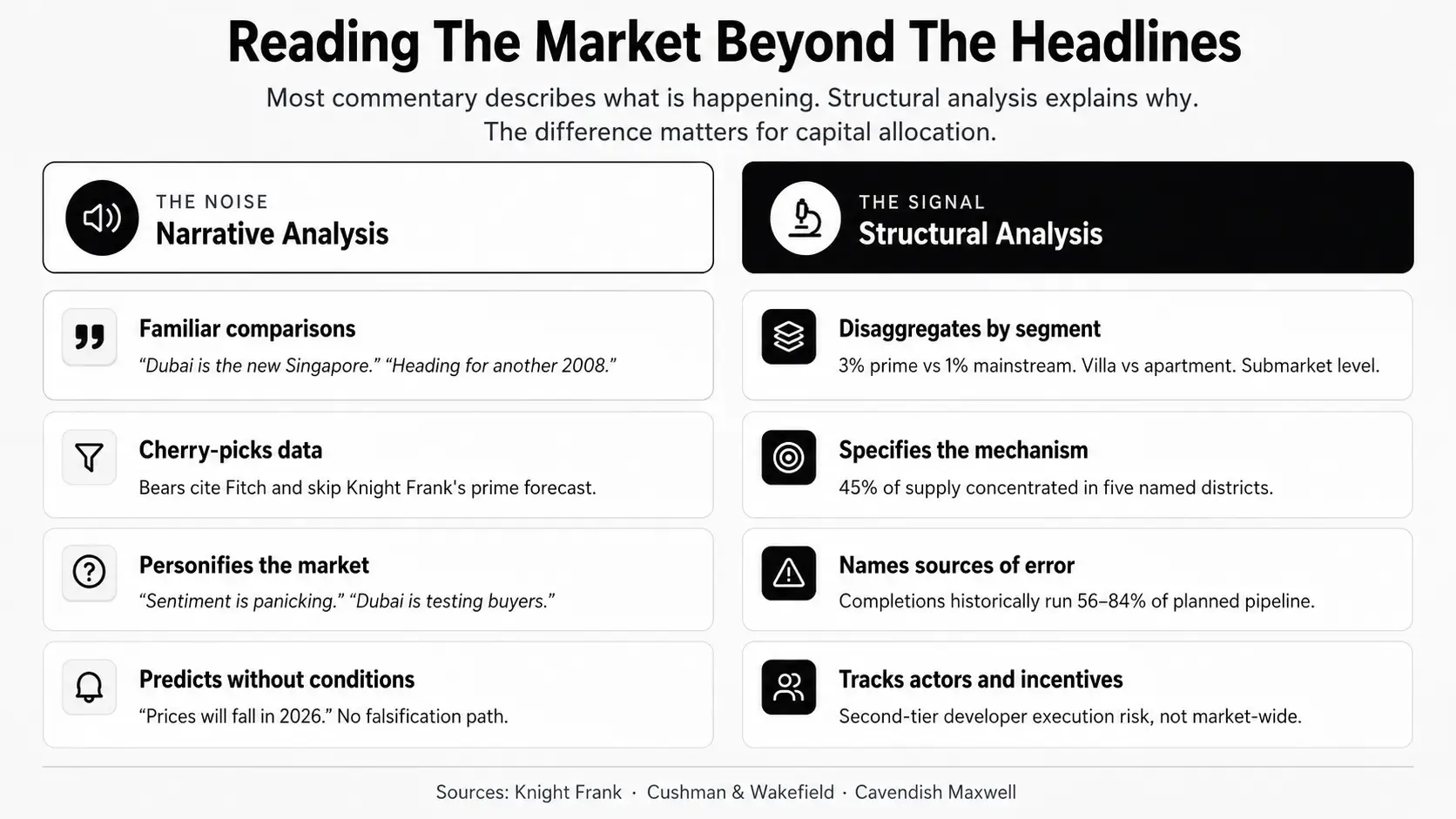

4. The institutional research is mostly good

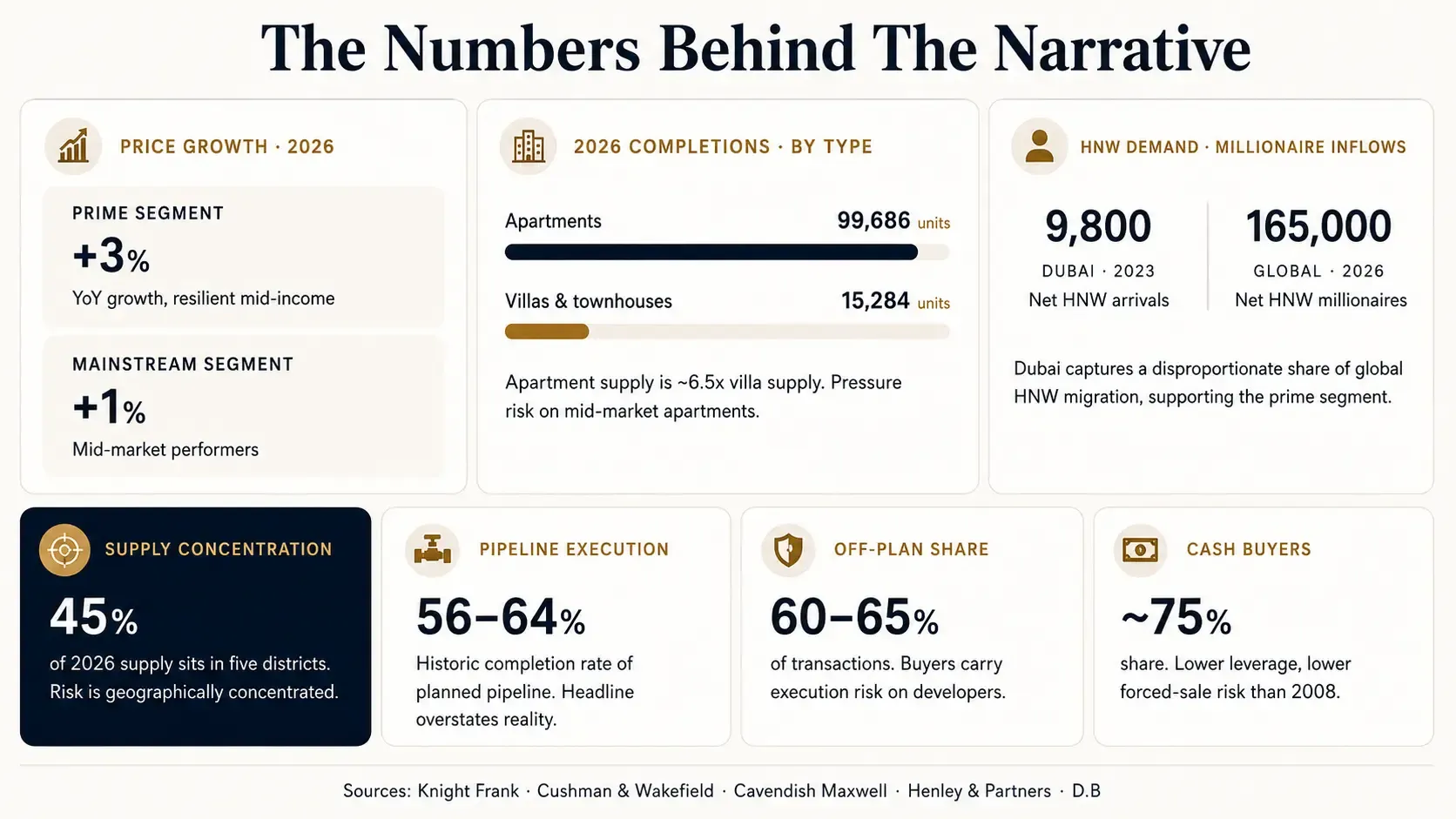

Institutional sources, Knight Frank, Cushman & Wakefield, Cavendish Maxwell, JLL, CBRE, the major banks, the Dubai Land Department itself, are largely doing structural analysis. They disaggregate, they specify mechanisms, they cite their assumptions, and they update on new data. They are not perfect. Each has its own framing biases, and aggregating multiple institutional views generally produces a better picture than relying on any single one. But the institutional research forms the analytical backbone for any serious Dubai allocation.

The mistake retail investors make is not that they ignore institutional research. It is that they consume it through narrative filters. A Knight Frank report saying "3% prime growth, 1% mainstream" gets compressed in social media commentary to "Dubai prices to rise." The disaggregation, which is the entire point of the analysis, gets stripped out in transmission. By the time the institutional view reaches the retail investor, it has been simplified into a narrative claim that contains very little of the original information. The same investor would be considerably better informed reading the Knight Frank report directly than reading three social media summaries of it. The institutional research is publicly available, free, and structurally rigorous. Most retail investors do not read it.

5. The narrative sources, calibrated

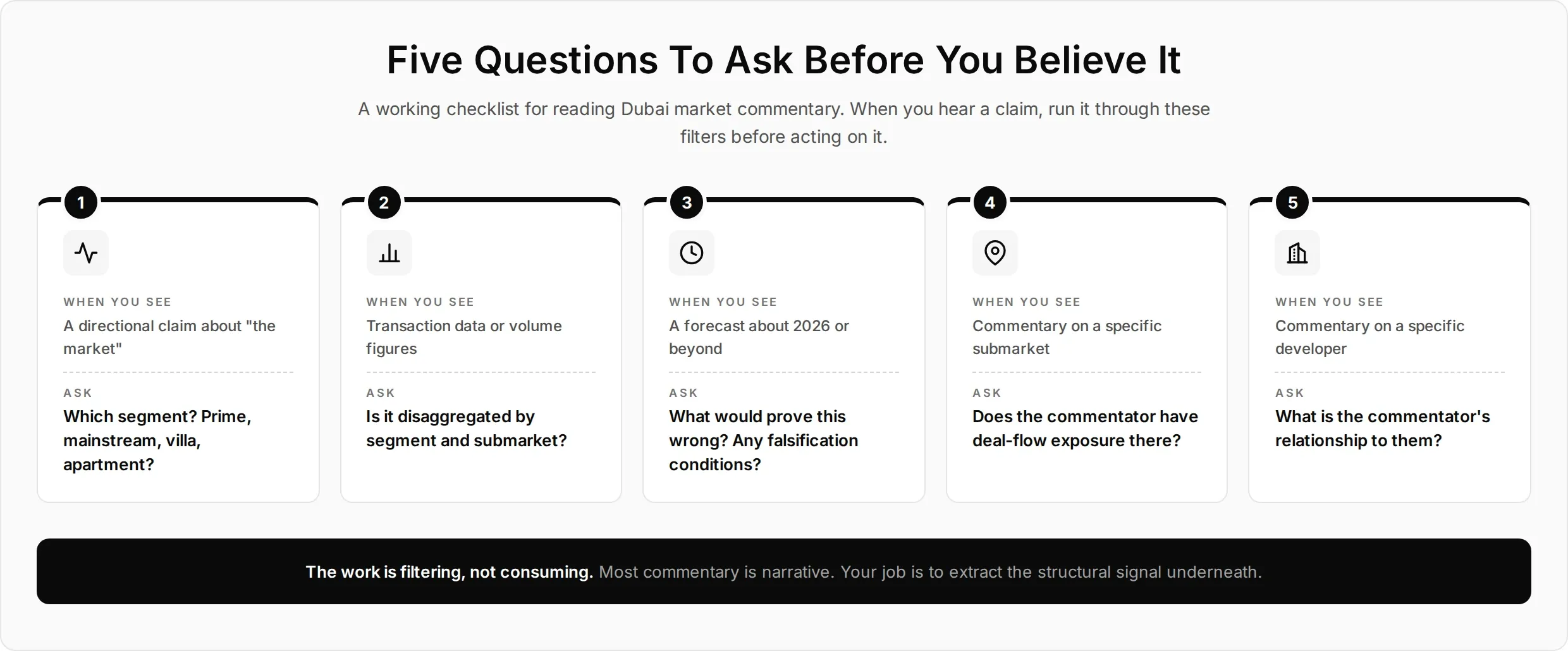

Public narrative sources, social media commentary, broker thought leadership, mainstream business press, are not useless. They surface anecdotes that institutional research does not capture, including granular submarket dynamics, specific developer behaviours, real-time deal flow patterns, and rapidly changing seller motivation profiles. They can be valuable for context. But they need to be consumed with calibration. A few specific filters that work in practice. Pay attention to who has skin in the game. A broker actively transacting in the market is closer to live information than a commentator who is not. A developer's representative talking about their own pipeline is more reliable than the same person commenting on competitors. A lawyer working on actual SPAs is closer to the regulatory reality than a generalist.

Track who has been right and wrong over multiple cycles. The most useful filter for narrative sources is their track record across the 2018-2020 softening, the 2020 COVID window, the 2022-2024 expansion, and the 2026 conflict period. Sources that called these correctly in real time are signal. Sources that consistently over-call corrections or expansion are noise.

Watch for narrative inversion. When the same source pivots aggressively from bullish to bearish or back, often within months, in response to news flow, that source is reactive rather than analytical. They are reading the market, not analysing it. Reactive sources can be entertaining and they can occasionally be right, but they are not building a coherent structural picture you can act on.

Discount predictions that lack falsification conditions. A bullish source that predicts "prices will rise" without specifying what would have to be true for that prediction to be wrong is producing a non-falsifiable claim, which is closer to marketing than analysis. The same applies to bearish sources predicting collapse without conditions.