Buy Dubai Real Estate from India 2026: LRS & Golden Visa Guide

Table of Contents

A structured advisory for discerning Indian investors & NRI family offices.

In the last financial year, Indian investors deployed approximately ₹3,173 crore (USD 389 million) into Dubai real estate, a 17% year-on-year increase. This flow is not incidental. It reflects a deliberate and accelerating strategic allocation by India's wealthiest families and capital structures toward a market that offers tax efficiency, legal transparency, USD-pegged stability, and a regulatory environment that increasingly rewards long-term capital. For family offices, institutional mandates, and principal investors seeking credible international diversification, understanding the mechanics of this market is no longer optional, it is foundational.

The Regulatory Gateway (FEMA Compliance & the LRS Framework)

Dual Jurisdiction: How the Architecture Works

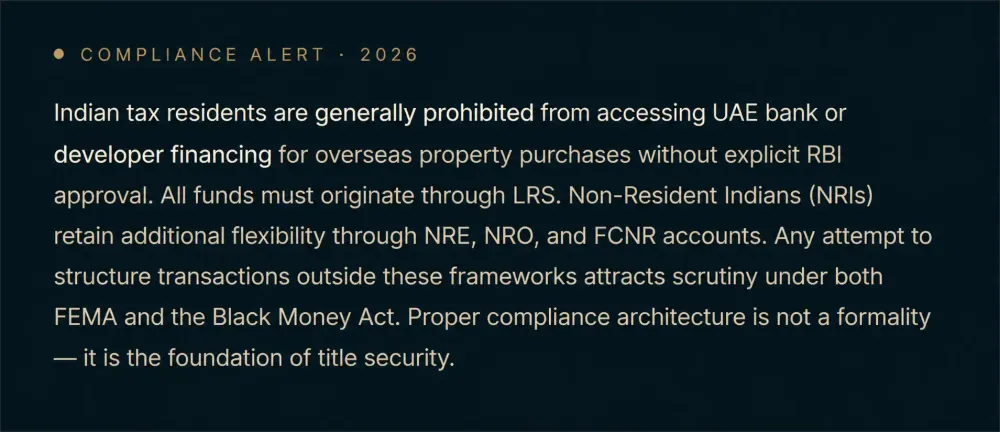

Cross-border property acquisition by Indian nationals operates within two concurrent legal frameworks. In the UAE, a 2006 freehold legislation grants foreign nationals 100% ownership rights in designated freehold zones, no local sponsorship, no residency requirement. In India, the Reserve Bank of India's Liberalised Remittance Scheme (LRS) governs the quantum and mechanics of outward capital flow for overseas real estate. Understanding how these two systems interact is the starting point of any well-structured transaction.

The USD 250,000 Annual Limit: What It Means in Practice

The LRS ceiling applies per individual, per financial year. For investments above this threshold, capital may be pooled across qualifying family members, each remitting independently through their own LRS entitlement. All outward transfers must be routed through an authorised dealer bank using purpose code S0005. Amounts exceeding USD 100,000 may attract 20% Tax Collected at Source (TCS) unless Forms 15CA and 15CB are filed correctly and in advance. Rental income and capital gains arising from the Dubai asset must be disclosed in the Indian Income Tax Return under Schedule FA (Foreign Assets).

Market Magnitude (Q1 2026 Transaction Intelligence)

A Record Opening Quarter

Dubai's property market posted its strongest first quarter on record. The data is unambiguous: 47,996 transactions were registered in Q1 2026, totalling AED 176.7 billion in value representing a 5.5% increase in volume and a 23.4% increase in value year-on-year. Price appreciation, not just volume, is the dominant story.

Segment Composition

Off-plan properties accounted for approximately 70% of all registered transactions a structural indicator of conviction in forward-looking demand. The luxury segment, defined as assets priced above AED 10 million, registered 2,076 transactions with a combined value of AED 43.7 billion; villas alone contributed 73% of this figure. Indian buyers maintained their position as the single largest foreign investor cohort at 18–20% of total market share.

Dubai's Q1 2026 performance is not a cyclical headline. It is evidence of a structurally repriced market with deep international demand, compressed supply and sovereign-level institutional confidence.

Branded Residences (The Institutional Asset Class)

A Market Growing at Scale

Dubai's branded residence segment is not a niche, it is an emerging asset class with institutional characteristics. Approximately 250 projects are currently in development, and the segment is projected to expand by 80% by 2030. These assets command price premiums of 30–60% over non-branded equivalents, driven by brand assurance, professional management and internationally recognised service standards. For family office mandates requiring both capital preservation and yield generation, this segment merits primary consideration.

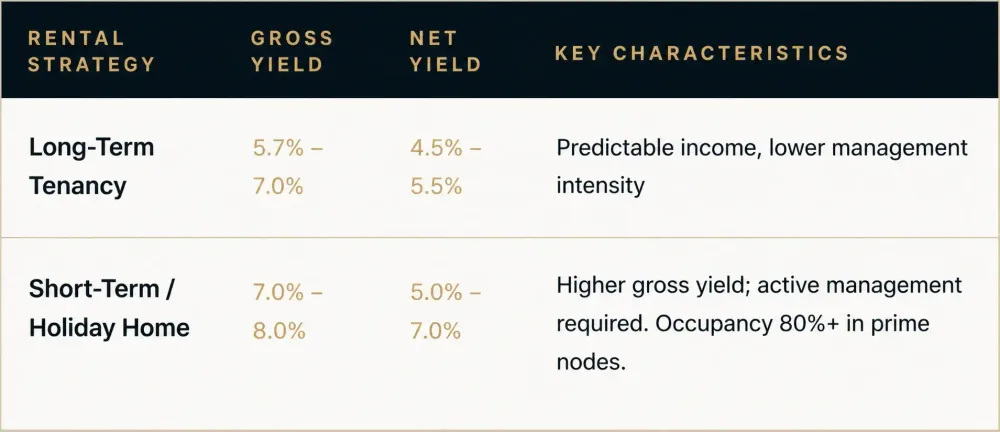

Yield Performance by Strategy

Occupancy rates in branded holiday home product consistently exceed 80% across prime locations including Downtown Dubai, Dubai Marina, Palm Jumeirah, and Business Bay. The combination of yield, occupancy, and premium pricing makes this category disproportionately attractive relative to comparable assets in London, Singapore or New York.

The Golden Visa Framework (Residency Through Real Estate)

Investment Thresholds

What Residency Confers

The Golden Visa confers UAE residency not citizenship. For Indian HNIs, the practical benefits are substantial: access to UAE banking infrastructure, comprehensive healthcare, the ability to sponsor immediate family members and an internationally recognised residency status that simplifies global mobility. For principals with multi-jurisdictional family structures, it provides a stable, tax-neutral base of operations. Critically, the visa does not require the investor to relinquish Indian tax residency, though this must be structured with appropriate professional guidance.

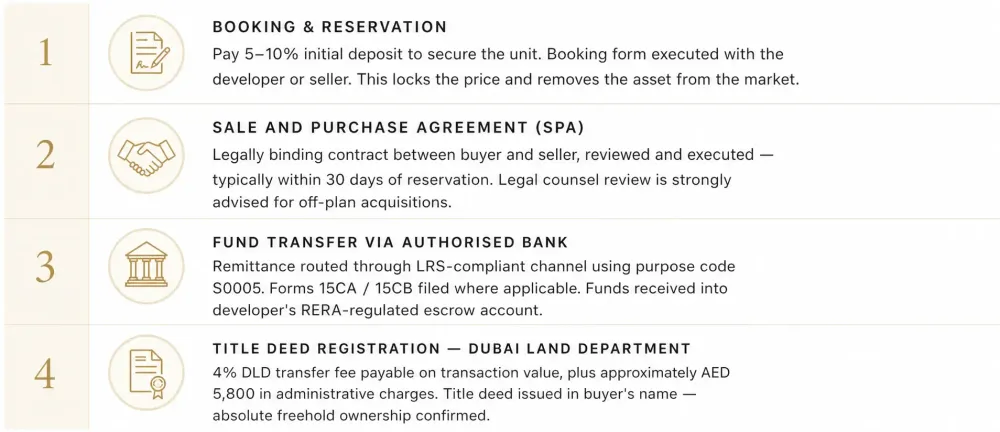

Transaction Mechanics (Acquisition Cost Structure)

The Four-Stage Purchase Process

Tax Treatment (India & UAE: A Comparative Framework)

India and the UAE operate under a Double Tax Avoidance Agreement (DTAA), which provides meaningful relief on dual taxation of income. Investors should engage both a UAE-licensed legal advisor and a qualified Indian Chartered Accountant before structuring repatriation of income or proceeds.

Short-Term Rental Strategy (Yield Optimisation in Prime Locations)

High-Yield Nodes

Properties in Downtown Dubai,Dubai Marina, Jumeirah Beach Residence (JBR), and Business Bay consistently generate 20–30% higher yields through short-term holiday home operations compared with long-term tenancy models. Net returns in these markets typically range between 5–7% after management fees, DEWA, and operational expenses. At scale, a portfolio approach across two or three of these nodes with professional property management delivers income stability alongside capital appreciation exposure.

The short-term rental market in Dubai is regulated by the Dubai Department of Economy and Tourism (DET), which provides a transparent licensing framework. Properties must be registered and host licenses obtained, a process that is efficient and well-supported by established management operators.

Institutional Considerations (Family Office & Multi-Asset Mandates)

Structural Advantages for Institutional Capital

-

Liquidity depth: Dubai's buyer pool spans 200+ nationalities. Off-plan secondary transactions are active and liquid, supported by developer resale mechanisms and a robust brokerage infrastructure.

-

Escrow protection: All off-plan developer funds are held in RERA-regulated escrow accounts, released only upon verified construction milestones. This provides institutional-grade capital protection absent in many emerging markets.

-

Infrastructure investment: Government capital expenditure on transport (Blue Line metro expansion), healthcare, and education underpins long-term demand fundamentals beyond any single developer cycle.

-

Regulatory predictability: Dubai Land Department reforms, freehold legislation, and the 2040 Urban Master Plan provide a credible multi-decade planning horizon for capital allocation.

-

Portfolio scalability: Multiple asset classes branded residences, villa communities, commercial, hospitality allow a family office to construct diversified UAE real estate exposure within a single jurisdiction.

Risk Assessment (Mitigation Considerations)

Dubai real estate in 2026 presents a convergence of conditions rarely available in a single market: no income tax, no capital gains tax, USD pegged currency stability, institutional-grade legal infrastructure, and a sovereign growth agenda with capital committed through 2040. For Indian HNI, UHNI and family office investors, this is not a speculative trade. It is a strategic allocation to a market that has structurally repriced and where the underlying drivers remain firmly intact. The question is not whether to allocate. The question is how to structure it correctly.

Read More

Bvlgari, One Za'abeel, Dorchester - Why Dubai Is Becoming the Global Capital of Branded Living

JP Morgan's $20 Billion Gulf Bet: What It Means for Dubai Property Investors

Dubai Property Replacement Cost 2026: Why Today's Prices Are Tomorrow's Floor