Luxury vs Mid-Market Dubai 2026: Which Delivers Better Returns?

Dubai property investment 2026: luxury vs mid market analysis covering rental yields, capital appreciation, villa supply, and risk-adjusted returns for HNW investors.

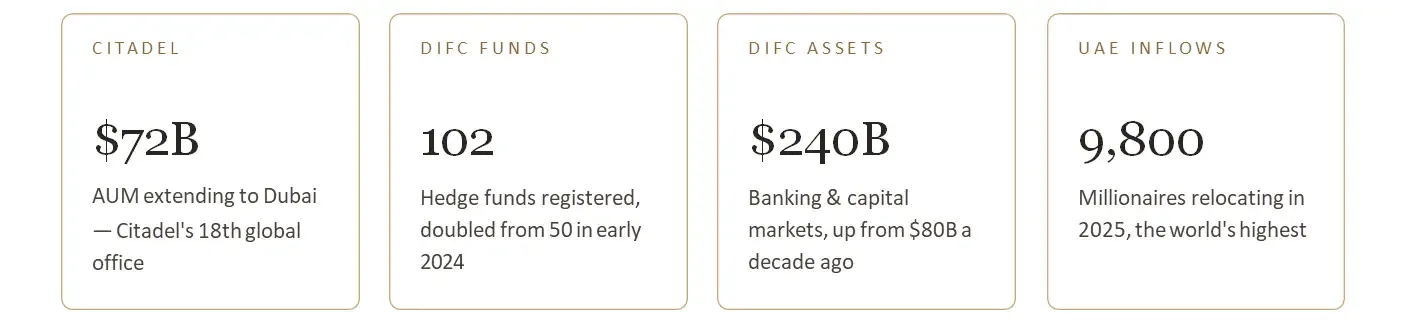

Ken Griffin's Citadel announced in December that it's opening a Dubai office in 2026. Most of the coverage zeroed in on the firm itself. $72 billion under management. An 18th global location. The last big hedge fund holdout in the UAE finally moving in. Fine. But that's not the part I'd lead with if you're holding property here. The question I keep coming back to is what kind of city now wins this sort of decision, and what that says about where Dubai real estate is heading over the next ten years.

A small detail in the Citadel announcement matters more than the headline. Their first team into Dubai is Fixed Income and Macro. Trading. Not a token presence. They want 24-hour coverage and tighter access to regional capital. Citadel didn't pick Dubai because it's having a moment. They picked it because the time zone, capital base and talent finally make a permanent seat here pencil out.

The number that stopped me wasn't $72 billion. It was 102. That's how many hedge funds are now registered at DIFC. Start of 2024 it was 50. Eighty-one of them manage over a billion dollars each. The 2025 arrivals read like a roll call: BlueCrest, Oak Hill Advisors, Silver Point, Squarepoint, Select Equity. Sitting alongside BlackRock, Brevan Howard, Millennium, ExodusPoint, Hudson Bay, Balyasny. DIFC is now in the global top five for hedge funds. Two years ago that sentence would have sounded ambitious.

Pull back from hedge funds and the picture only gets bigger. DIFC crossed 8,000 active companies in 2025. It now employs over 50,000 working professionals and added 4,100 jobs in a single year. Wealth and asset management firms have grown past 470. Banking and capital markets count 289 firms with nearly $240 billion in assets. Foundations have jumped to 842, family-related entities are over 1,250, and office occupancy is essentially full. They're building 1.6 million square feet of new commercial real estate Dubai supply right now, and the planned Zaabeel District expansion is sized for 42,000 companies and 125,000 working professionals.

Take DIFC alone. It goes from 50,000 today to a planned 125,000. Roughly 75,000 extra finance, fintech and asset management professionals, all packed into one district. Assume one home per 1.5 working professionals (conservative, because senior bankers usually come with a spouse and family rather than a flatmate) and you get around 50,000 net new homes pulled in by DIFC's expansion alone. Before anyone counts the hospitality jobs, the schools, the lawyers and accountants who follow institutional money around.

Layer that on top of a market that's already tight. Dubai passed 3.9 million residents in 2025. Q1 transactions were up 23 per cent year on year, mostly off plan dubai launches. Private market firms running over $700 billion are already operating in the UAE, including EQT, Eurazeo, Baron Capital and Silver Point. Citadel isn't a one-off. It's the latest name to land on a base that's been building for years.

Hedge fund principals, portfolio managers, family office heads. They don't behave like the buyer who built Dubai's last cycle. The earlier waves were visa-led mid-market buyers, off-plan flippers and lifestyle migrants, and a lot of them did very well. The new wave is different. These are people picking Dubai over London, Geneva or Singapore largely for tax and operational reasons. They land with budgets that compress quickly into a small handful of communities. And once they're here they buy fast.

Watch the premium end first. Senior fund people don't rent for three years while they figure things out. They buy. Emirates Hills. Dubai Hills villas. Palm Jumeirah villas. Al Barari, District One, the gated parts of MBR City. These are the names that come up over and over when I'm working with this profile, and they consistently rank among the best villa communities in Dubai for it. Supply is structurally limited, so when a hundred new senior families show up looking simultaneously, prices move. The Dh50–150 million bracket, basically Dubai mansions, saw the strongest velocity in a decade through 2024 and 2025. Luxury villas for sale in Dubai are now competing for a buyer pool deeper than I've seen it. Honestly, luxury real estate Dubai at the very top is a supply problem now, not a demand one.

The second wave goes into branded waterfront and serviced product. Bluewaters, Emaar Beachfront, Dubai Marina apartments, Downtown, Business Bay. This is where younger relocators and single executives end up. Luxury apartments in Dubai with proper rental management, a recognisable brand, and ten or fifteen minutes to DIFC outperform raw land here, because that buyer doesn't want a project. They want something that runs itself if they get redeployed to Hong Kong for a year. Buy penthouse in Dubai searches have gone vertical, particularly for waterfront apartments dubai inside Emaar properties, where luxury penthouses in Dubai sell to people who want brand, hotel-grade service and a clean exit.

Then there's the third wave, and this one's already showing up in the data. DIFC-adjacent rentals. Two and three-bed units inside a fifteen-minute commute. Downtown Dubai apartments, Business Bay apartments for sale, Dubai Hills apartments, Dubai Creek Harbour residences, the new Wasl1 corridor. Yields there are already running ahead of the citywide average. I'd expect that gap to widen, not close.

Capital doesn't move to a city just because the tax is friendly. It moves when the city is visibly building out the infrastructure to absorb it. The Dh34 billion Gold Line metro, completing 2032, will connect Mina Rashid, Business Bay, MBR City, Meydan, Al Barsha South and JVC, with an Etihad Rail interchange built in. The Blue Line in 2029 opens up Dubai Creek Harbour and Silicon Oasis. Al Maktoum International is being scaled up to take over as the city's main airport. New projects in Dubai across the off plan property pipeline, particularly Emaar projects in Beachfront, The Valley, Dubai Hills and Emaar South, are increasingly priced against this trajectory rather than today's snapshot. None of it was built because Citadel was coming. All of it was already committed. Citadel and the firms behind them are arriving precisely because all of it is now visible.

1. Capital migration is a slow trade. Citadel announced in December 2025. The office opens in 2026. Hiring runs into 2027. The housing demand from those hires won't show up in a single quarter. It builds in waves over two and three years. Which is why Dubai investment real estate keeps absorbing capital even when monthly Dubai real estate prices look like they're going sideways.

2. Location specificity is doing more work than community. A villa in Dubai Hills with a five-minute drive to a Gold Line station, a school catchment that suits an international family, and a layout that actually works for a senior banker is not the same asset as one half a kilometre away missing any of those. Pricing inside the same community will keep separating.

3. Read the inflows alongside the outflows. The 102 DIFC hedge funds, $700 billion of private-market firms in the UAE, and 9,800 incoming millionaires are not three separate stories. They're one story. UK non-dom changes, US state-level tax pressure, European regulatory drift, all pushing the same way. Textbox 26, TextboxReading Dubai real estate news in isolation right now is reading half the picture

Citadel on its own is one decision by one firm. Read it next to the rest, though, the doubling of DIFC's hedge fund count, the 1.6 million square feet of commercial space under construction, the Zaabeel plan for 125,000 working people, a UAE that's now the world's leading destination for millionaire migration, and the picture shifts. Dubai has gone from being an interesting alternative in the calculus of global finance to being the default. Real estate companies in Dubai working with senior institutional and expatriate buyers will define this cycle, the way developers defined the last one.

The right thing to do is not to buy something just because it sits inside a DIFC catchment. The right thing to do is to factor capital migration into a wider view of community, micro-location, building, and timing. The investors who read these maps early tend to hold the better assets when the cycle matures. The investors who wait until the news is comfortable usually arrive after the move.

Rakhi Megchiani Sales Director · Xperience Realty

Dubai property investment 2026: luxury vs mid market analysis covering rental yields, capital appreciation, villa supply, and risk-adjusted returns for HNW investors.

Dubai’s property market continues its upward trajectory, crossing AED 252 billion in Q1 2026 transactions. Explore the latest market insights and opportunities with Xperience Realty.

Secondary or off-plan in Dubai 2026? Compare ROI, risks, payment plans, and resale potential in this investor's guide to making the smarter property choice.