5. The European cohort

The European cohort is broader and more fragmented than the UK or Russian cohorts. It includes French HNWs responding to wealth tax pressure, Italian HNWs hedging political and currency uncertainty, German entrepreneurs relocating after liquidity events, Scandinavian wealth holders responding to inheritance tax pressure, and Benelux-based principals diversifying domicile. Per Henley, France saw a projected -800 millionaire outflow in 2025, Spain -500, Germany -400. Italy saw a +3,600 inflow at the destination level, indicating that European HNW migration is not just one-way out, but the Dubai-bound subset is meaningful and growing.

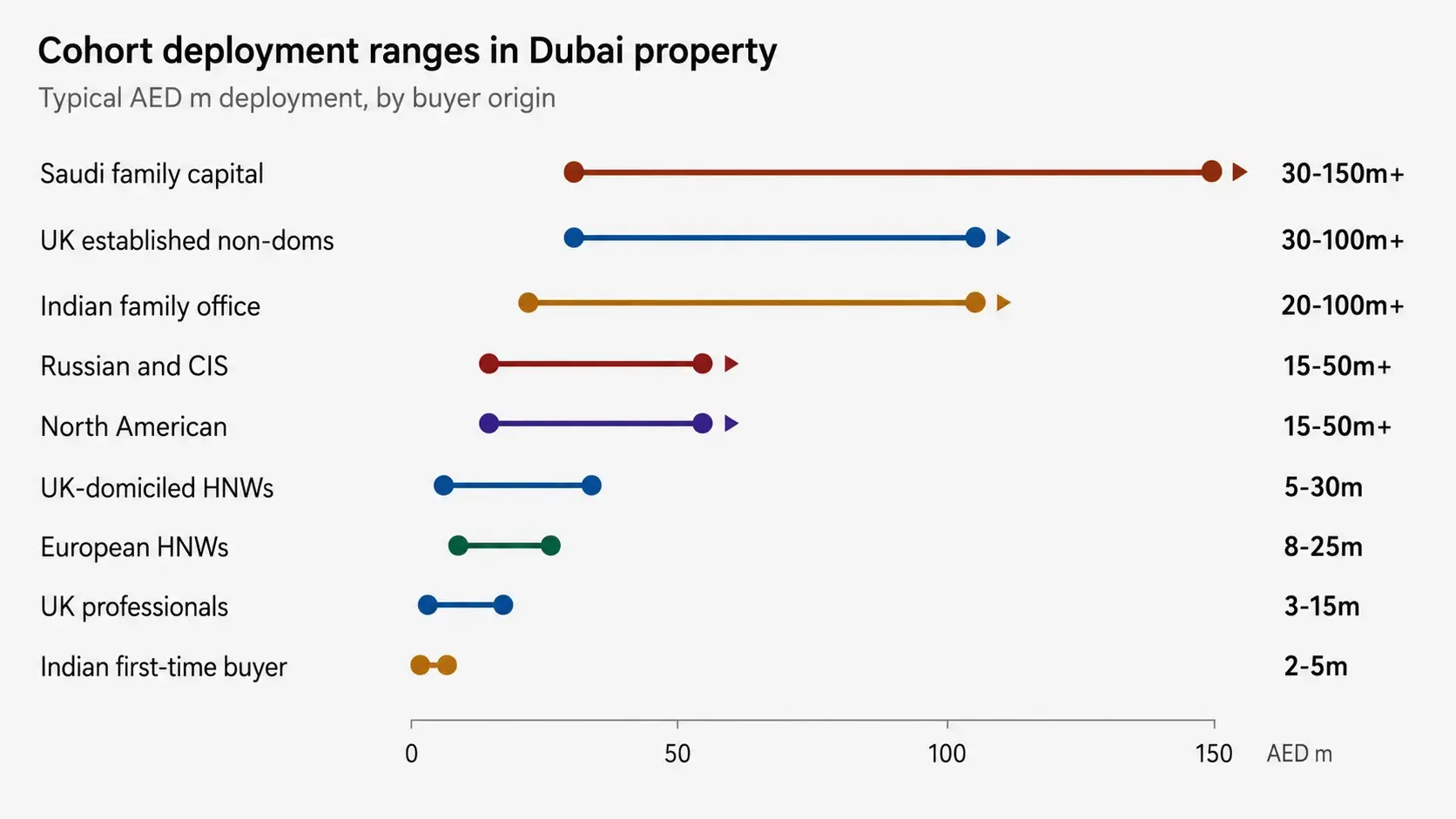

Buyer profile is more lifestyle-anchored than the UK cohort. Many European HNWs are not making the full residency switch but are establishing a Dubai base for winter months, regional business, and family flexibility. Deployment levels typically AED 8-25m. Asset preference skews toward branded residences (Bvlgari, One Za'abeel) and prime apartment product in Dubai Marina, Downtown, and Bluewaters. Villa preference is narrower, often concentrating in Palm Jumeirah for the lifestyle profile.

The European cohort's importance for the Dubai market is qualitative rather than quantitative. They legitimise the market for other Western buyers, anchor the cultural and culinary infrastructure (the high-end restaurant, hospitality, and lifestyle layer that supports prime market positioning), and provide a steady demand floor for branded residence and waterfront product.

6. The North American cohort

The North American cohort is smaller in headcount than the others but disproportionate in deployment size when active. Henley projected the US to attract a +7,500 net millionaire inflow in 2025, indicating that the US is itself a destination market, not primarily a source. Active US buyers in Dubai are typically tech entrepreneurs, finance principals, or family offices with specific Dubai-based commercial activity.

Buyer profile skews toward investment positioning rather than residency relocation. The US tax system's worldwide taxation framework means full residency relocation produces limited tax benefit unless paired with citizenship renunciation, which most US HNWs are not pursuing. The Dubai allocation is therefore typically positioned as a portfolio diversification and optional-residence asset rather than a primary base. Deployment levels are concentrated, often AED 15-50m+, into prime waterfront, branded residence, and trophy villa positions. The Canadian subcohort is more active relative to size, reflecting Canadian capital gains and inheritance pressures and the presence of a meaningful Indian Canadian and South Asian Canadian buyer pool with cultural and family ties to the region.