FCNR Deposits at 7% vs Dubai Property: What UAE-Based NRIs Should Know in 2026 | Archana Bhan

Table of Contents

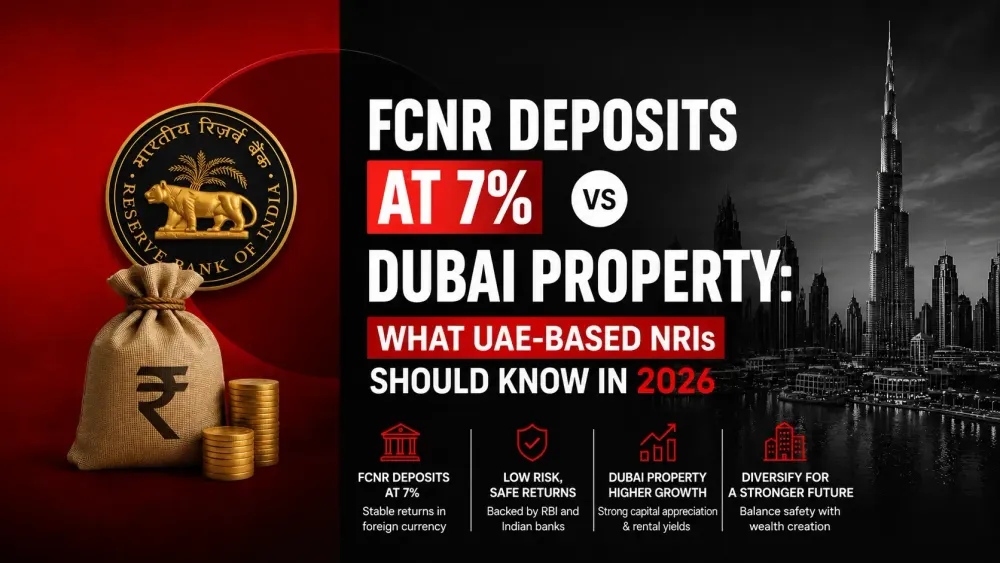

India's FCNR deposits now pay up to 7.1% in USD. A UAE-based advisor explains who should take it, the fine print, and how it compares with Dubai property. India just offered its diaspora 7% on their dollars and if you live in the UAE, this deal rewards you more than almost any NRI on the planet. But before you move a single dirham, it's worth reading the fine print that the headlines skip.

I'm a RERA-certified real estate professional with over eleven years in the Dubai market and a law degree behind me, and I'll tell you upfront: some of what follows argues against my own industry's short-term interest. That's deliberate. My clients build long-term wealth, and long-term wealth is built on the whole picture not the half that sells.

What India Actually Announced

On 5 June 2026, the Reserve Bank of India made a move it hadn't made in nearly thirteen years. It agreed to absorb a cost banks normally carry themselves hedging a dollar deposit against rupee depreciation, historically worth roughly 3.5% of interest per year. Relieved of that cost, banks passed the savings to depositors. The result: FCNR (Foreign Currency Non-Resident) dollar deposit rates jumped from around 3.35% in May to 6–7.1% by mid-June. State Bank of India moved to as high as 6%, Canara Bank to 6.5%, and AU Small Finance Bank to 7.1% (Reuters; Gulf News, June 2026).

The mechanics matter. An FCNR deposit is held, paid, and returned in US dollars. Whatever the rupee does and it touched roughly 96.84 to the dollar in May (FBIL data, via Reuters) — your capital never converts, so it never feels the currency move. Dollars in, dollars out. One correction to the popular framing, though: "no rupee risk" is not the same phrase as "no risk." The deposit carries a lock-in and liquidity constraints, covered below.

Why India Made This Move and Why It Deserves Respect

Early 2026 put pressure on every oil-importing economy. Conflict in West Asia pushed crude past $100 a barrel, and import-heavy currencies across Asia felt it. India's response was notable for what it didn't do: it didn't hike rates and choke growth. Instead, it invited diaspora capital in on genuinely attractive terms supporting the rupee and strengthening reserves while paying NRIs a real dollar rate.

RBI Governor Sanjay Malhotra said the scheme would let banks raise rates for non-resident depositors and that the central bank expected "healthy and large-scale inflows" (RBI policy statement, June 2026). Banks estimate the window could attract $35–40 billion (Reuters). That is a confident economy leaning on a structural strength, its global diaspora not a shaky one bracing for the worst.

The UAE Advantage: Tax-Free at Both Ends

Here is the part that matters most to our clients, and the part few channels explain.

-

FCNR interest is tax-free in India for non-residents. But your country of residence can still tax it. An NRI in the United States declares that interest to the IRS, one published worked example showed a headline 7% shrinking below 4.7% after tax (InvestMates, 2026). The UK taxes it. Canada taxes it.

-

A UAE resident pays no personal income tax. So for you, the deposit is tax-free in India and tax-free where you live, tax-free at both ends. The same product, the same rate, lands fuller in your pocket than anywhere else in the diaspora.

-

For capital you cannot afford to lose, money you want parked safely in dollars for several years , FCNR right now is one of the cleanest homes available. That is not a grudging admission; it's a recommendation for the right bucket of money.

The Fine Print the Hype Skips

Two things to know before you act.

The "17–27% returns" are not the deposit. Some brokerages have promoted double-digit FCNR returns (Business Standard, June 2026). Those figures come from leverage, borrowing dollars abroad, gearing up several times your own capital, and depositing the borrowed sum to capture the rate spread. The strategy stands on borrowed money, a thin spread, and floating borrowing costs. The clean, unleveraged deposit pays 6–7%. The rest is debt dressed as yield.

The deposit has house rules. Funds are locked for a minimum of one year; early withdrawal forfeits interest, and even after a year an early exit typically costs about a percentage point (Gulf News, June 2026). Tenors run three to five years, and the current window closes on 30 September 2026. Acting inside the window is reasonable, acting because someone else's urgency became your panic is not.

FCNR vs Dubai Property: The Floor and the Ceiling

Now the comparison you'd expect a real estate firm to rush. We'd rather do it honestly, because the two are not rivals, they're two ends of one portfolio.

-

What investors love about FCNR, dollars, tax efficiency, real yield, Dubai property also offers. The dirham has been pegged to the US dollar since 1997, so a Dubai asset is effectively dollar-denominated. The UAE levies no capital gains tax and no tax on rental income. And prime communities generate rental yields broadly in the same 6–8% band as the deposit (Knight Frank / CBRE).

-

The difference is the ceiling. A deposit's 7% is a cap; it will never pay more. Property earns rent and can appreciate. It can be lived in, leveraged prudently, and passed to the next generation and at AED 2 million it qualifies the owner for a 10-year UAE Golden Visa.

-

An illustration, not a promise: an AED 2 million off-plan unit at 20% down commits AED 400,000 of equity. If the market appreciates 25% over three years ([DATA CHECK: DLD historical appreciation data]) and the unit generates roughly AED 120,000 in net rent, the combined gain approaches AED 620,000 on AED 400,000 deployed, tax-free. The same AED 400,000 in an FCNR deposit earns approximately AED 72,000 of interest over the period. Safe, certain, and capped.

The honest caveats, equally clearly: the property scenario depends on market performance and on holding through the cycle. The 20% down payment is leverage, secured against a hard asset, but leverage nonetheless. Property is less liquid than a deposit. Off-plan carries handover and developer risk, which is why we work exclusively with track-record developers and RERA-escrowed projects. Markets move in cycles; anyone who says otherwise is selling, not advising. One instrument guards wealth. The other grows it. Well-built portfolios in this region typically hold both, deliberately.

A Practical Framework

The advice we give across the desk, in four steps. First, split your capital into two honest buckets: money to keep safe and money to grow, different jobs, different homes. Second, for the safe bucket, the plain (unleveraged) FCNR deposit merits serious consideration before 30 September, particularly for UAE residents. Third, for the growth bucket, weigh Dubai property on its real merits a dollar-pegged, tax-free, ownable asset with genuine upside and risks you accept with open eyes. Fourth, before signing anything, consult a chartered accountant on your residency status and a market specialist on the asset.

This article is investor education, not personalised financial, legal, or tax advice. Deposit rates, market data, and visa thresholds change; verify current figures before acting. ROI figures are illustrative scenarios, not guarantees. Sources: Reuters, RBI, Gulf News, Business Standard (macro/FCNR); Knight Frank, CBRE, DLD, RERA (Dubai market).

Frequently Asked Questions

An FCNR (Foreign Currency Non-Resident) deposit is a fixed deposit with an Indian bank held in foreign currency, typically US dollars, available to NRIs and OCIs. Because it is held and repaid in dollars, the depositor carries no rupee conversion risk on capital or interest.

FCNR interest is tax-free in India for non-residents, and the UAE levies no personal income tax — so for UAE tax residents the interest is generally tax-free at both ends. Confirm your individual position with a chartered accountant.

They serve different purposes. FCNR offers capital protection and a fixed, capped dollar return; Dubai property offers rental yield plus potential appreciation, Golden Visa eligibility at AED 2 million, and inheritance value — with market, liquidity, and developer risk. Most balanced portfolios use both.

The enhanced-rate scheme runs until 30 September 2026. Rates vary by bank and tenor; verify current rates directly with the bank before committing.

Read More

When to Buy Dubai Property in 2026: Timing vs Positioning

Why Buyers Are Moving from Dubai Marina to Dubai Creek Harbour

Bvlgari, One Za'abeel, Dorchester - Why Dubai Is Becoming the Global Capital of Branded Living