Why Dubai Holding’s $6.5 Billion Stake in Emaar Matters for Your Property Portfolio

Dubai Holding just paid $6.5B for 29.73% of Emaar. Government money is now anchoring Dubai's biggest developer. Here's what it means for your portfolio.

Knight Frank tracks over 160,000 units in Dubai's 2026 registered pipeline, while Cushman & Wakefield expects realistic 2026 deliveries closer to 55,000 units after applying historical completion rates.

Dubai's 2025 completion rate hit 64 percent of planned (39,700 of approximately 62,000 units) per Knight Frank's Shehzad Jamal, with the long-term completion rate near 36,000 homes per year.

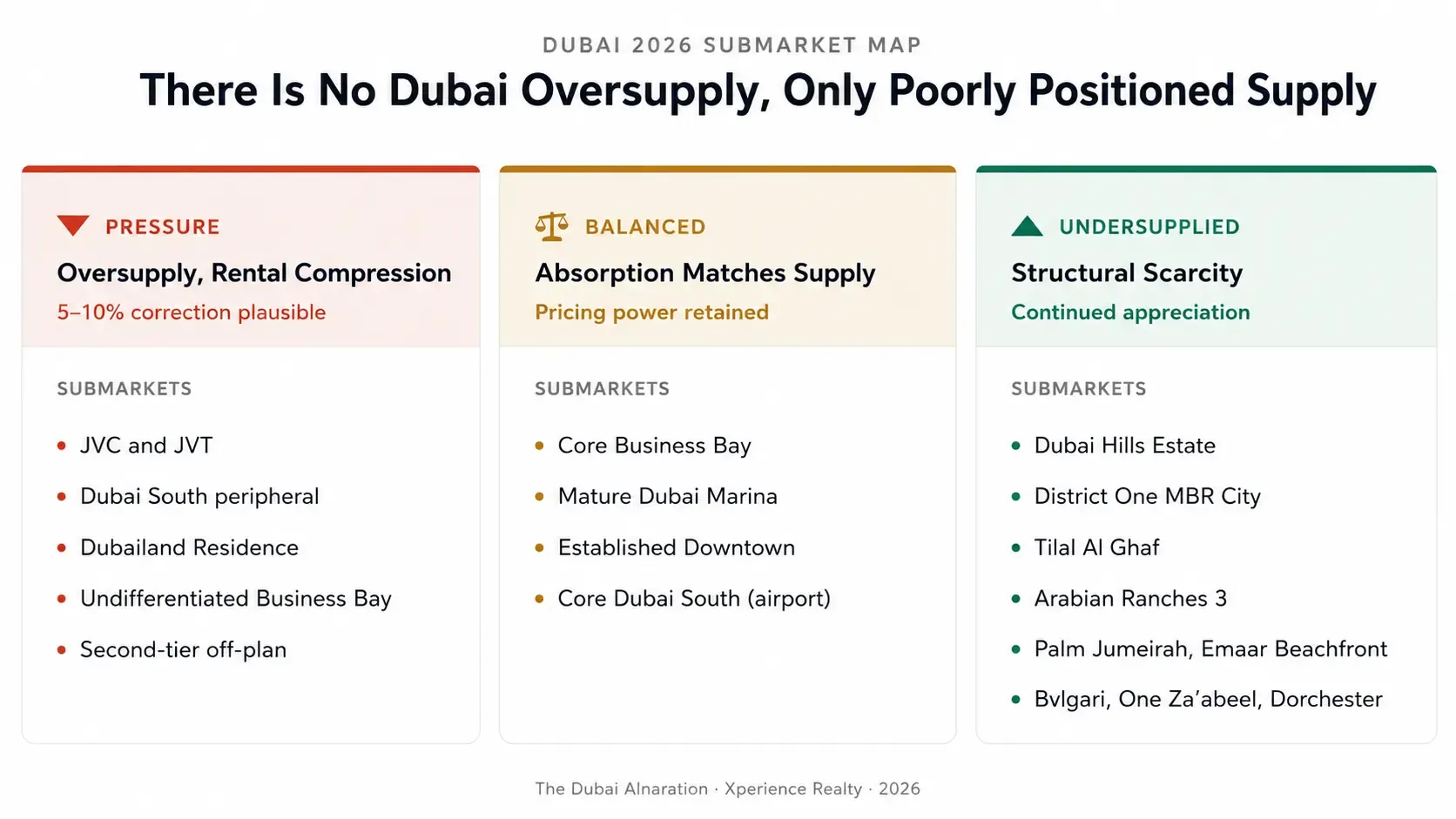

Cushman & Wakefield indicates 45 percent of all under-construction stock concentrates in five districts: JVC and JVT, Dubai South, MBR City, Business Bay, and Dubailand Residence Complex.

Only 15,284 villas are scheduled for 2026 delivery against 99,686 apartments, with the 2027 villa pipeline tighter at 5,631 units, creating a structural villa shortage.

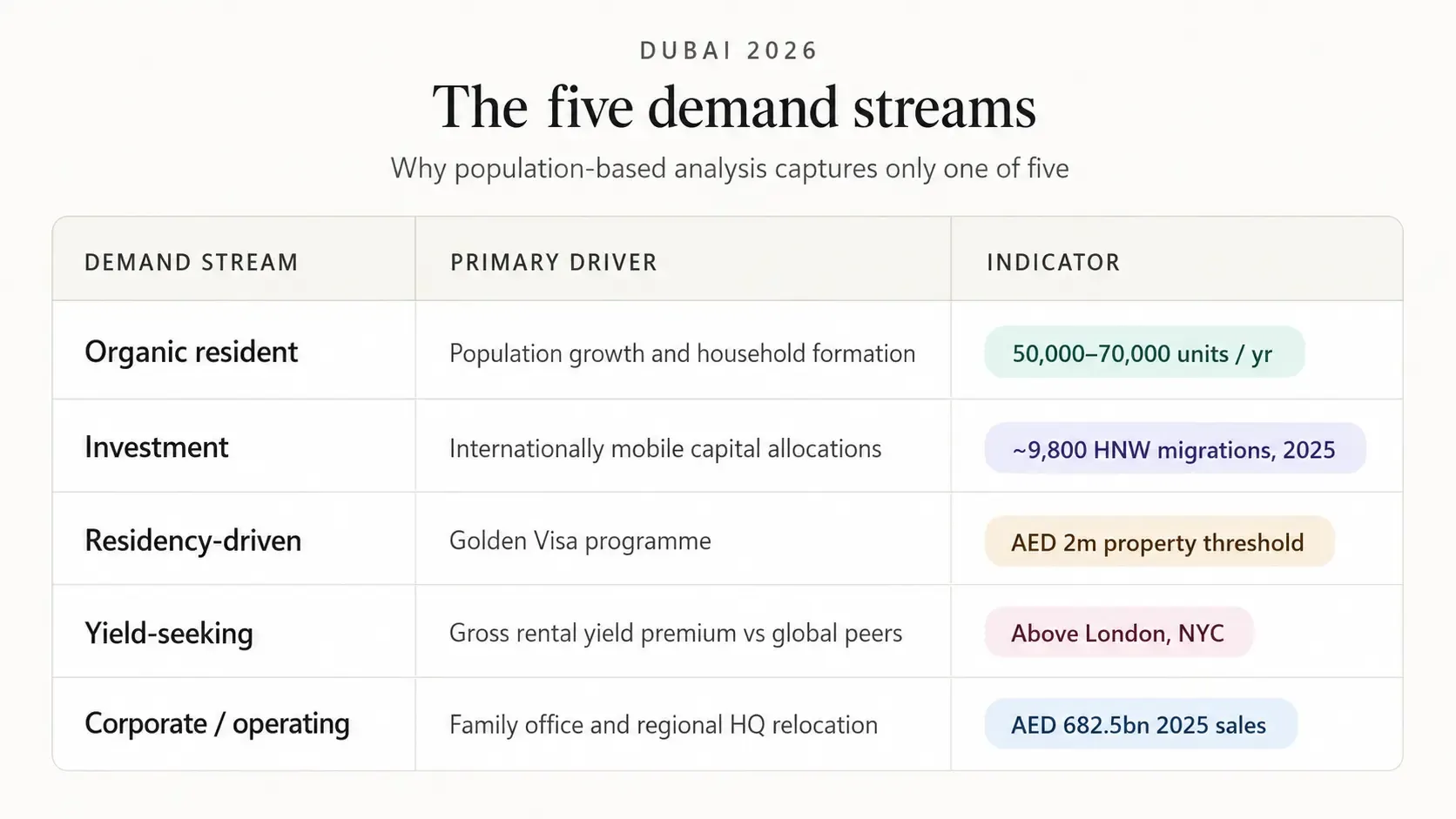

Dubai's organic resident demand alone absorbs 50,000 to 70,000 units per year, with additional demand from HNW migration, residency driven buyers, and yield-seeking capital.

Every cycle, the same narrative comes back. Dubai is building too much. There will be oversupply. Prices will collapse. It sounds intuitive. You look at cranes across the skyline. You see launch events every week. You read headlines about 120,000 or 160,000 or 200,000 units entering the market.

This logic is incomplete in a way that matters. The oversupply argument rests on a single analytical assumption: that supply and demand operate uniformly across the market. They do not. Dubai is not a single market with a single supply curve and a single demand curve. It is multiple overlapping markets with very different supply elasticities very different demand profiles and very different absorption dynamics.

A more accurate framing: Dubai does not have an oversupply problem. It has a supply distribution problem. The better question is not how much is being built, but what is being built, where it is being built, and who it is being built for.

Knight Frank's pipeline tracking suggests over 160,000 units could enter the market in 2026 on a registered basis, with around 331,000 residential units potentially completed between 2026 and 2030 in a best case scenario assuming 70% delivery on registered starts. Cushman & Wakefield's view, after allowing for delays, is that 2026 actual deliveries will be closer to 55,000 units. Property Monitor data via Cavendish Maxwell shows around 366,000 residential units projected to enter the market by 2028, with concentration in 2026-2027.

These are large numbers. The long term historical completion rate is approximately 36,000 homes per year. Even conservative realistic estimates put 2026 deliveries at 1.5 to 2x that average. If you stop there, the oversupply narrative looks reasonable. The aggregate numbers mislead because they combine at least five demand streams that are distinct and because supply itself is not distributed in the way the headline suggests.

Most Western analysis assumes demand equals population multiplied by household formation rate. That assumption breaks for Dubai. Five distinct streams feed transaction volume, responding to different variables.

Even with a pessimistic demand view, the oversupply argument fails because supply itself is not uniformly distributed. The market breaks cleanly into high elastic and low elastic segments, priced on completely different physics.

High elastic supply is where developers can and do build quickly. Apartments in investor-heavy zones, in high density communities, at mid market price points. Knight Frank puts apartments at roughly 85% of the 2026 pipeline. Cushman & Wakefield indicates approximately 45% of all under construction stock concentrates in just five districts: JVC and JVT, Dubai South, MBR City, Business Bay, and Dubailand Residence Complex.

Low elastic supply is where developers cannot increase inventory quickly. Prime villas, waterfront product, land constrained communities, branded residences. Only 15,284 villas are scheduled for 2026 against 99,686 apartments, a roughly 6:1 ratio that widens further in 2027 with only 5,631 villas. Dubai has a potential oversupply of high elastic apartment stock in specific mid market corridors. Dubai has a genuine undersupply of low elastic prime and villa product. These are not the same market.

The biggest analytical error retail commentary makes is treating Dubai as a unit of analysis. For supply and demand work, the correct unit is the submarket.

Completion is the number of units delivered. Absorption is the number actually purchased, occupied, and active in the market. The oversupply narrative implicitly assumes completion and absorption will diverge sharply in 2026-27. The data suggests otherwise.

Dubai's completion rate is consistently below registered pipeline. Knight Frank's Shehzad Jamal confirmed 2025 completions hit 64% of planned (39,700 of around 62,000 registered units), a meaningful improvement over the 2022-2024 rate of approximately 56% (97,000 of 174,000 projected). The formal 2026 pipeline of 91,500 to 160,000+ units will realistically translate to 50,000-70,000 actual deliveries. Cushman & Wakefield's specific estimate is closer to 55,000.

Absorption capacity is stronger than most models capture because it includes multiple demand streams. Organic resident demand alone absorbs 50,000-70,000 units per year. Absorption is also elastic upward, when supply arrives at attractive pricing, it pulls forward demand that would have waited. Likely 2026 arithmetic: approximately 50,000-65,000 realistic completions against roughly 60,000-90,000 units of absorption capacity across all five streams. A market that absorbs its supply, not one that collapses under it. The caveat: this citywide arithmetic hides the submarket-specific imbalances. Absorption works in aggregate. It will not protect individual JVC studios from rental compression.

Even pessimistic oversupply scenarios run into an economic constraint most analysis ignores. Developers cannot keep building indefinitely at current price points. Construction materials and labour, land acquisition in prime submarkets, and developer financing are all rising. Every new launch enters at a higher embedded cost base. Prime Emaar Beachfront launches in 2020-21 priced at approximately AED 2,200 per sq ft; Knight Frank's Q3 2025 prime average sat at AED 3,767 per sq ft. Replacement cost on comparable beachfront is structurally above AED 2,900 per sq ft before margin. In a market with rising cost floors, apparent oversupply has a built in governor.

Developers also manage supply strategically. Pipelines are not delivery schedules. Three mechanisms matter. Phased releases, a 3,000 unit project rarely means 3,000 units hitting the market simultaneously. Launch timing, major developers routinely delay formal launches by six to twelve months in response to absorption signals. Inventory controls, even within launched projects, developers hold back stock from initial release. Planned supply overstates actual supply by 30-50%. The 160,000 unit 2026 pipeline is not a schedule. It is a ceiling, with a realistic mid-case closer to 55,000-65,000.

Fitch projects a moderate correction of up to 15% through 2H 2025 and 2026, driven by approximately 210,000 units of new supply across 2025-2027 and assumed population growth of around 5%. Moody's forecasts moderate correction beginning late 2026. Citi's tail-risk requires population growth to collapse from 4% to 1%. Each gets the genuine submarket pressure right. Each overstates the generalisation.

Fitch's 5% population assumption is conservative against actual 6%+ growth, a small input error compounds through the supply demand ratio. Moody's completion benchmark actually undermines the severe oversupply case. Citi's tail risk requires a genuinely implausible reduction in growth with no observable catalyst. The March 2026 conflict produced no net outflow, and Goldman's data showed villa prices up 16% YoY through that exact window. None of this means the bear case is wrong. It means the bear case is directionally right about submarket pressure and market wide wrong about severity. A 5-10% correction in the most exposed apartment clusters is plausible and does not contradict the structural thesis.

Dubai is not at risk of systemic oversupply. The aggregate arithmetic works. The 2026-27 wave will be absorbed. Specific assets are at risk, undifferentiated mid market apartment stock in JVC, Dubai South peripheral corridors, less distinguished Business Bay clusters, Dubailand, second tier developer off plan in supply heavy zones. Low elastic supply segments face the opposite problem. Villa inventory in Dubai Hills Estate, District One, Tilal Al Ghaf. Prime waterfront at Palm Jumeirah, Emaar Beachfront. Branded residence product. The 2026 villa pipeline of 15,284 units is not enough to shift the balance in established family communities.

There is no such thing as Dubai oversupply. There is only poorly positioned supply, concentrated in specific clusters, which will correct selectively while structurally undersupplied segments continue to appreciate. The market will not correct uniformly. It will sort itself. If you are evaluating Dubai based on total supply numbers, you are looking at the wrong data. The better question is not how much is being built. It is where supply is increasing, and where demand has already outpaced it.

Dubai Holding just paid $6.5B for 29.73% of Emaar. Government money is now anchoring Dubai's biggest developer. Here's what it means for your portfolio.

Discover the best off-plan projects in Dubai for 2026. Expert breakdown of trusted developers, smart communities, and the investment risks nobody talks about.

Explore the best waterfront properties in Dubai for Indian investors. Expert insights on top communities, rental yields, Golden Visa benefits, and smart investment opportunities.